|

According to a report by AlixPartners, the global Aerospace and Defense (A&D) industry spent close to $126 billion on 436 M&A transactions in 2018. 2019 is set to be another record year, led by the recently announced merger of United Technologies and Raytheon, expected to have a combined market value of $166 billion.

Global defense spending is up 2.6%, with the US alone accounting for 36% of the total, or $634 billion, up 4.6%. The US is set to increase its defense budget by another 7% in 2019 (FY2020). Spending in Europe was up 2.6%, while Central and Eastern Europe (excl. Russia) spent 13% more than in 2017. A clear weak spot in the defense sector was helicopters, with total deliveries in 2018 down 10.6% to 1,520 and far below 2014 levels, when oil prices were above $100/barrel.

1 Comment

Aerospace & Defense private equity investor Acorn Growth Companies has announced the acquisition of DIMO Corp., a supplier primarily of military aircraft parts. Rick Nagel, Managing Partner of Acorn Growth Companies, has stated: “DIMO’s global operating infrastructure and key relationships with foreign government aerospace and defense procurement organizations will be a tremendous strategic asset to the Acorn portfolio.” Terms of the transaction were not disclosed publicly. Sohrab Naghshineh, DIMO’s founder, will continue to serve as its President and will also take on a role assisting other Acorn portfolio companies with international business development opportunities.

In an interview with Association for Corporate Growth National Capital, Ricky White, Partner at RyanSharkey, says that Government contracting still drives the majority of M&A activity in the Mid-Atlantic region.

On March 28, White will chair ACG’s Mid-Atlantic Growth Conference at the Hyatt Regency Tyson’s Corner.

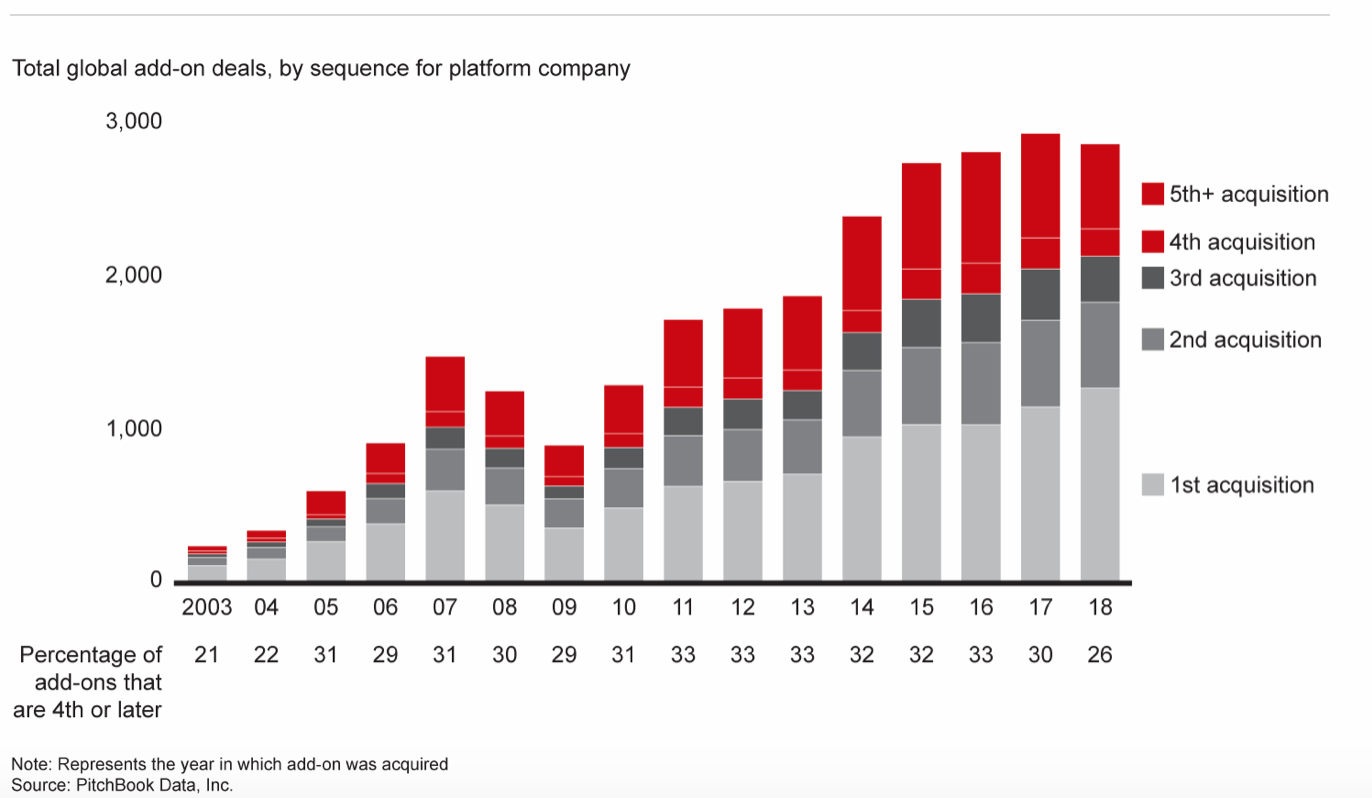

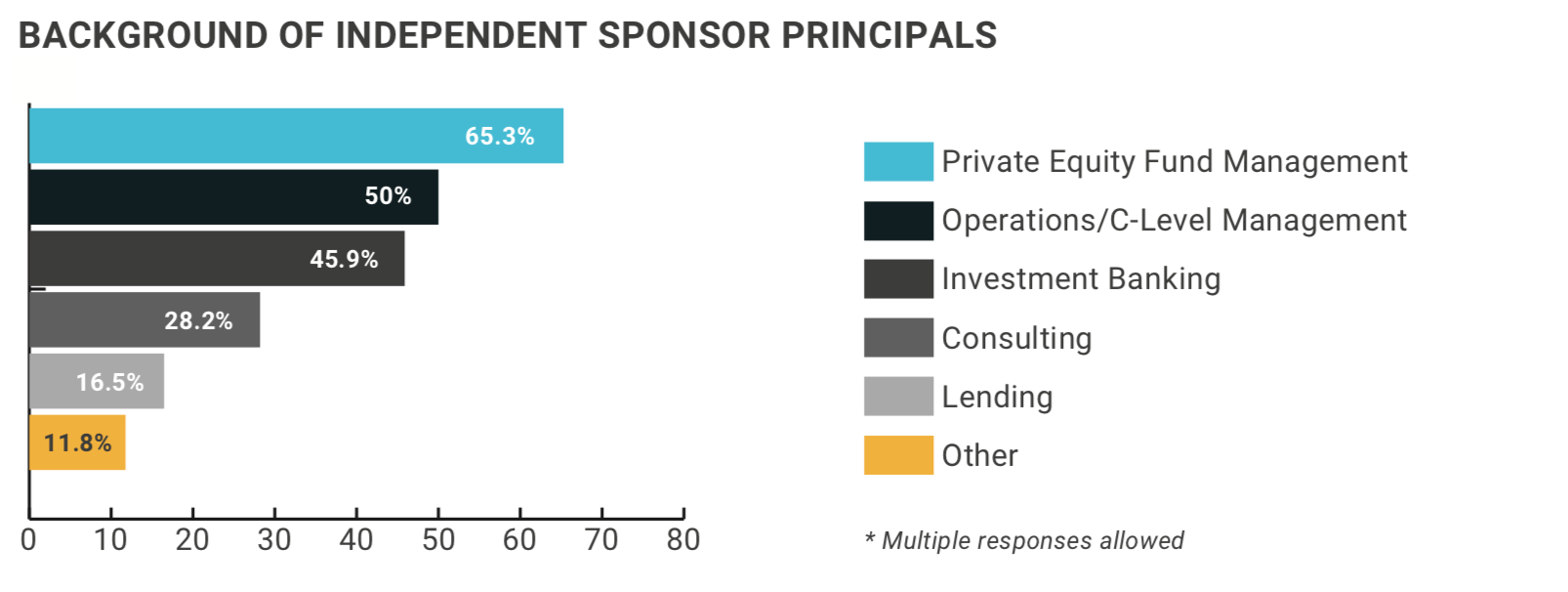

An article on Axial points to growing value from buy and build strategies. The article quotes Gretchen Perkins from Huron Capital: "Pursuing a buy-and-build strategy and employing add-on acquisitions is a solid way to achieve above market growth and shareholder value in a 3% GDP environment” In growing markets with fragmented competitor landscapes, PE investors increasingly employ a buy and build strategy by first acquiring a "platform" company -- typically a larger company with established management team and operations -- and then add smaller acquisitions that tend to trade at lower multiples compared to larger companies. Bain Capital's 2019 Global Private Equity Report further defines the buy and build strategy not as just doing a couple add-ons, but a deliberate strategy with a steady pace of acquisitions: "We define buy-and-build as an explicit strategy for building value by using a well-positioned platform company to make at least four sequential add-on acquisitions of smaller companies." And increasingly, add-on details are part of an overall strategy based on M&A, as evidenced by the following table:  DFW Capital Partners has acquired a controlling stake in IT Services contractor Sev1Tech. “The Sev1Tech management team sought out DFW as a partner to enable growth both organically and through acquisition..." says Bob Lohfeld, CEO of Sev1Tech. From their public announcement: "Sev1Tech plans to leverage this investment to add new services, support new and existing customers and strengthen our mission capabilities." A 2018 survey and report by Citrin Copperman shows the continued growth and development of the independent sponsor model in private equity investing. Independent sponsors are gaining popularity due to their flexibility, focus on quality of individual investment opportunities, and strong alignment with capital partners. “YOU CAN’T PLAY PORTFOLIO THEORY WHEN YOU ARE AN INDEPENDENT SPONSOR. EVERY DEAL HAS TO STAND ON ITS OWN MERITS.” Most significantly, in our opinion, is the continued trend of independent sponsors with backgrounds in industry. The report shows that 50% of independent sponsor principals have a background in Operations/C-Level Management, as opposed to the earlier days of sponsors coming predominately from PE and IB backgrounds.  Success of the independent sponsor model has generated increased interest and even competition from capital providers, with strong participation from family office investors, especially early in the life of the sponsor. In fact, 70% of independent sponsors in their first 2 years of operations are working with family offices and high net worth individuals. By the time they are more than 5 years in operations, many still retain family office relationships but have brought on capital from traditional PE firms (41%) and Mezz Funds (51%).

Of course, independent sponsors, like their private equity counterparts, face the challenges of competition for deals in a sustained sellers' market, as well as the pressure of sufficient deal sourcing activities at attractive valuations despite the limited internal resources for independent sponsors. Many, though, will continue to thrive by focusing closely on a specific sector where the principals have a proven track record and an established professional network. With over 20 years of industry experience as senior operations executives, FRAMCOR makes direct investments and works as an independent sponsor for private equity investments into defense and government contractors providing critical professional services to the U.S. both domestically and overseas. See more about our investment focus here.  Triumph Group, Inc. (NYSE:TGI) has announced the sale of its Triumph Fabrications business units to aerospace and defense private equity firm Arlington Capital Partners. “Triumph Fabrications consists of four independent companies, which operate in five locations throughout the US. These sites encompass more than 1 million square feet of factory space dedicated to the aerospace industry by supporting complex sheet metal components and assemblies for fixed wing and rotorcraft platforms… Combined, the businesses generated revenues of approximately $150 million during Triumph Group’s fiscal year ended March 31, 2018.” An annual survey of 222 Aerospace and Defense Industry executives & experts by investment banking firm KippsDeSanto & Co shows expectations of continued strong sector growth and M&A activity. "Our 2019 survey results suggest continued strong mergers and acquisitions activity in the aerospace, defense, and government services sectors," says Managing Director Kevin DeSanto. Top priority areas for M&A include:

Wolf Den Associates has published its always informative Practitioner Perspectives for December 2018. Focused on the growing M&A market in federal contracting. Highlights include:

Cerberus has announced it will acquire a 70% stake in the defense unit of Navistar International (NYSE - NAV). Navistar announces quarterly earnings on Dec 18, and it will be interesting what details of the deal are offered by its Chairman and CEO Troy Clarke. Navistar hasn't regularly broken out its military sales in its earnings statements, preferring to report total sales for its Trucks and Parts divisions by truck class. For the first 9 months ending 31 July 2018, total Truck sales were up 23% due (partly) to an "increase in military sales." This increase probably has more to do with an industry-record total orders in the quarter of 52,000 Class 8 heavy trucks, up 34% compared to last year. But its medium truck class saw an increase in orders of 18% as well. Surely Clarke will have to outline the impact this sale has on its ongoing operations, and we should also get more details on valuation and terms than Cerberus has announced. It will also be interesting to see if this marks a trend in corporations spinning off their "non-core" defense units due to strength in that market.  |

Our ideasLatest FRAMCOR news and ideas on global defense and government contracting, major programs, strategy, talent management, M&A, and more. Archives

July 2019

Categories

All

|

RSS Feed

RSS Feed